Nuclear Supply Chains

The nuclear renaissance is not only a question of reactor design.

The supply chain is a critical factor in the deployment of advanced nuclear reactors.

Some vulnerabilities already exist [1-2]. Below are a few examples:

Uranium, from origin, mining, milling and conversion. Most uranium used in the United States (U.S.) is imported from Canada, Australia, Kazakhstan, Russia and Uzbekistan [3]. Conversion facilities are limited in the U.S. and are mainly operated in foreign countries including Canada, China, France and Russia (more constrained since August 2024).

High-Assay Low-Enriched Uranium (HALEU): HALEU is uranium enriched between 5% and 20% in U-235. A significant number of advanced reactors and SMRs are expected to require this fuel. The U.S. still has limited domestic infrastructure to produce and supply it at scale.

Graphite, a key material for neutron moderation in some reactor designs. The U.S. is mainly reliant on imports for graphite while a large share of global production is concentrated in China [4].

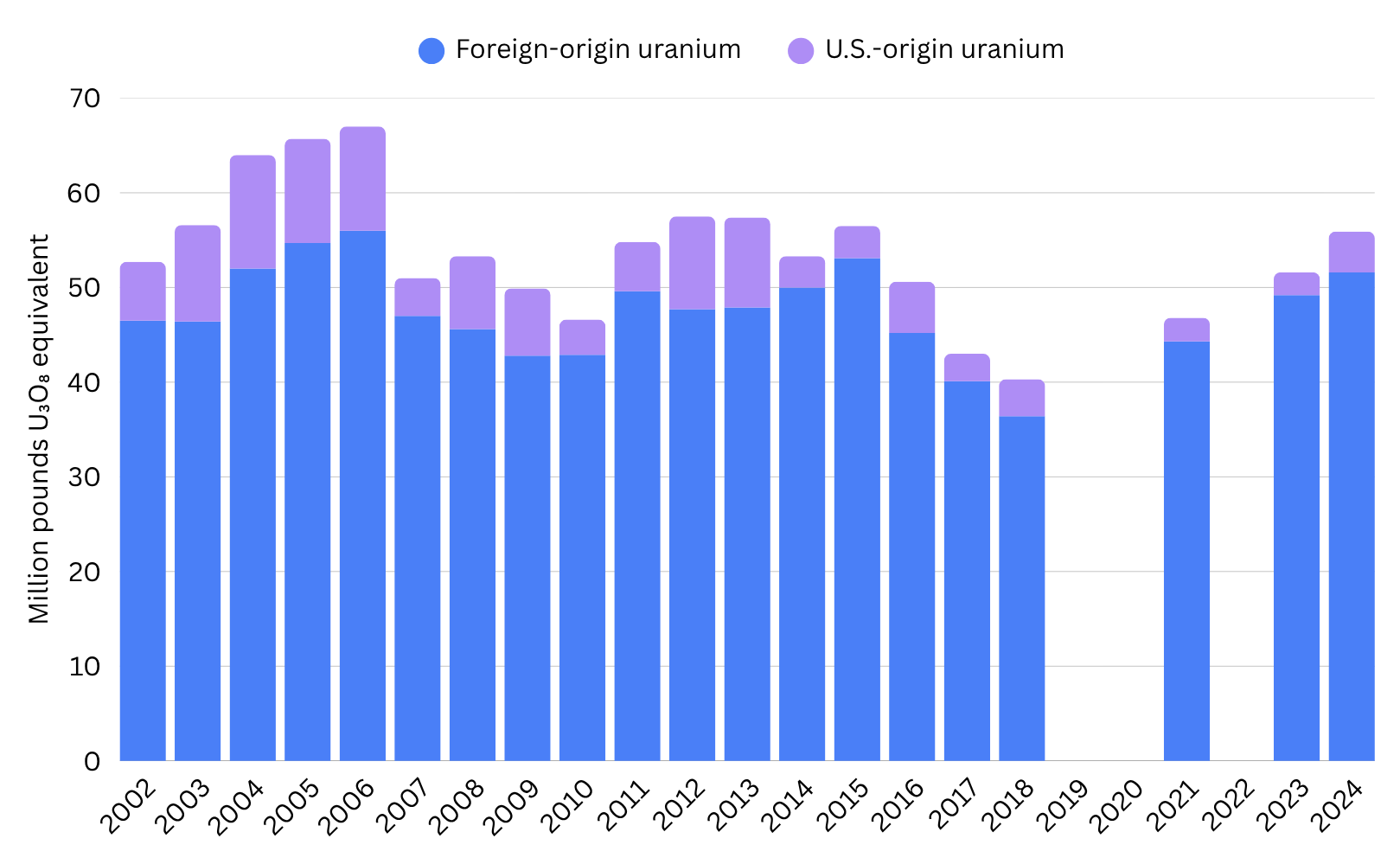

The broader fuel-cycle challenge begins upstream. As shown in Figure 1, U.S. civilian reactors have relied overwhelmingly on foreign-origin uranium for more than two decades. In 2024, foreign-origin uranium accounted for over 90% of total purchases, highlighting the structural dependence of the U.S. nuclear fuel cycle on international supply chains.

This dependence becomes even more critical when moving beyond uranium supply to enrichment capacity. The widening HALEU gap illustrates the scale of a challenge critical to advanced nuclear reactors.The Piketon demonstration facility in Ohio (U.S.) is expected to produce around 900 kilograms per year in the near term — against a projected domestic demand of 50 metric tons per year by 2035 [5] and a cumulative need of approximately 5,350 metric tons by 2050 under a net-zero emissions scenario [6]. Today, only Russia and China have the infrastructure to produce HALEU at commercial scale. Rosatom alone controls roughly 40% of global enrichment capacity [7] and the 2024 U.S. ban on Russian enriched uranium imports makes building domestic alternatives no longer optional.

Figure 1: U.S.-origin and foreign-origin uranium purchased by U.S. civilian nuclear power reactors, 2002–2024 (million pounds U₃O₈ equivalent).

Data Sources: U.S. Energy Information Administration: Uranium Industry Annual, Tables 10, 11 and 16, 2002. Form EIA-858, Uranium Marketing Annual Survey, 2002-2024.

In parallel, France’s Orano is expanding the Georges Besse II enrichment plant, with four additional centrifuge cascades expected by 2030 while the UK’s Urenco is developing a HALEU facility at Capenhurst expected to produce 10 tonnes annually by 2031 [8].

The problem is timing: new enrichment facilities typically take a few years to construct.

The speed of the nuclear renaissance may not be limited by technology alone but by supply-chain maturity.

In addition, the Payne Institute recently described nuclear and SMR non-fuel critical minerals as an emerging “fourth value chain” alongside clean energy, defense and AI/semiconductors [9]. The inclusion of uranium in the 2025 U.S. Critical Minerals List points in the same direction [10].

The question is no longer only whether advanced reactors and SMRs can work. It is whether the full ecosystem can deliver. The nuclear renaissance will depend on the resilience of the supply chain in order to maintain credibility, speed of development and growth.

Stratomic helps organizations assess nuclear supply-chain risks, identify strategic dependencies, and translate technical constraints into actionable decisions.

Stratomic. Where nuclear expertise meets strategic vision.

References

[1] U.S. Department of Energy, "Nuclear Energy Supply Chain Deep Dive Assessment", Feb. 2022.

[2] U.S. Department of Energy, "HALEU Frequently Asked Questions," Office of Nuclear Energy, accessed May 2026.

[3] U.S. Energy Information Administration, "U.S. nuclear generators import nearly all the uranium concentrate they use," Jan. 2025.

[4] J. Zhang, C. Liang and J. Dunn, "Graphite Flows in the U.S.: Insights into a Key Ingredient of Energy Transition," Environmental Science & Technology, vol. 57, no. 8, pp. 3402–3414, Feb. 2023, doi: 10.1021/acs.est.2c08655.

[5] U.S. Department of Energy, Office of Nuclear Energy, "What is High-Assay Low-Enriched Uranium (HALEU)?," Dec. 2024.

[6] B. Dixon et al., "Estimated HALEU Requirements for Advanced Reactors to Support a Net-Zero Emissions Economy by 2050," Idaho National Laboratory, INL/EXT-21-64913, Dec. 2021.

[7] M. Pir-Budagyan, "Securing Energy Independence: The US Path to Resilient Enriched Uranium Supply Chain," Atlantic Council, Feb. 2025.

[8] IAEA, "HALEU: Power for a New Generation of Reactors," IAEA Bulletin, vol. 67, no. 1, May. 2026.

[9] K. A. Bala and R. Johnston, "Nuclear and SMR Non-Fuel Critical Minerals Supply Chain: An Emerging Fourth Value Chain," Payne Institute for Public Policy, Colorado School of Mines, Mar. 2026.

[10] U.S. Geological Survey, "Interior Department releases final 2025 List of Critical Minerals," Nov. 2025.